The 1031 Variations

A DEFFERED Exchange —

If the Purchase of the Replacement Property is Delayed for a Permitted Period of Time AFTER

the Sale of the Relinquished Property; then, the QI is authorized to Hold the Sales Proceeds in Escrow

(an Insured Exchange Account for the benefit of the Taxpayer).

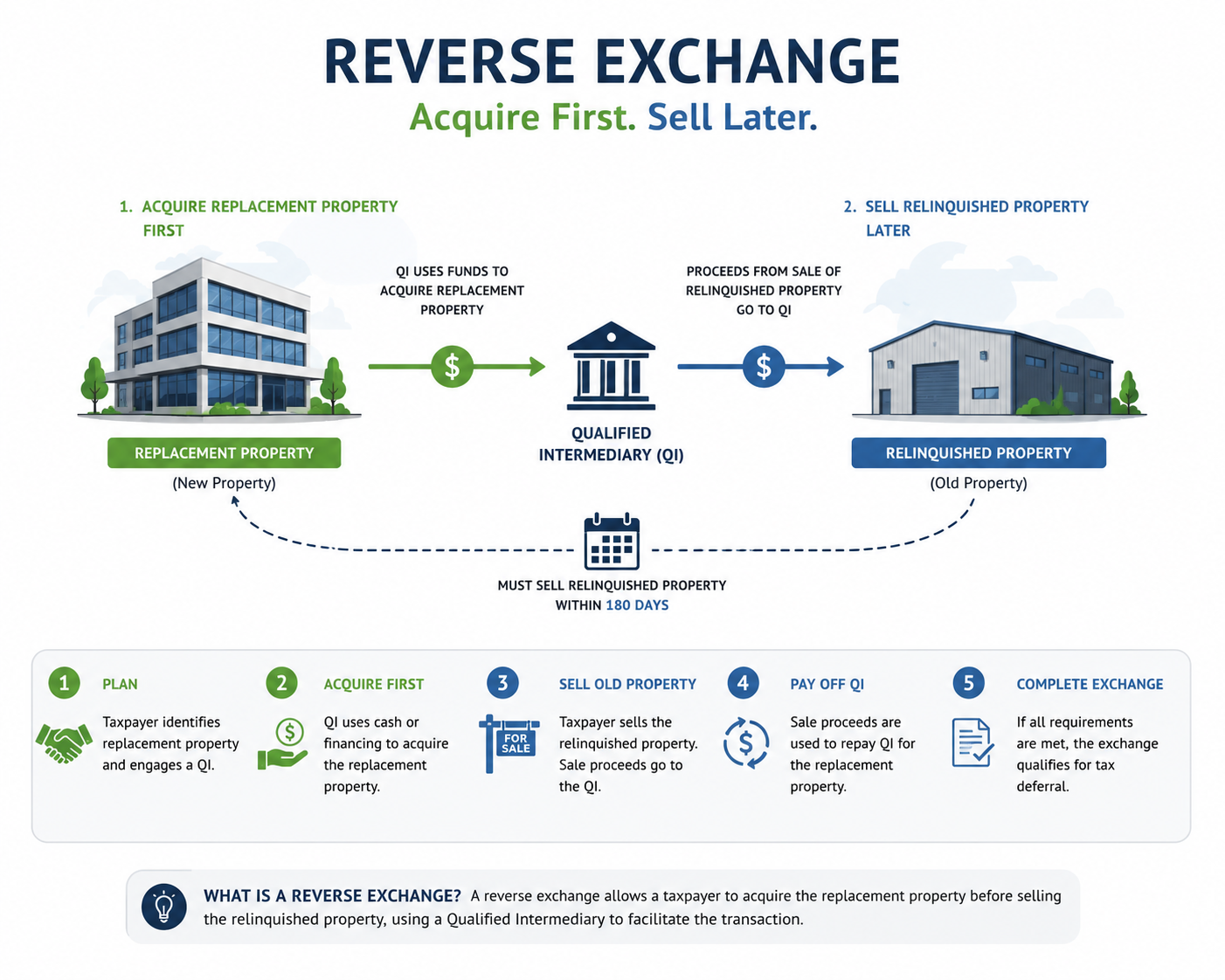

A REVERSE Exchange —

If the Purchase of the Replacement Property

must occur

BEFORE the Sale of the Relinquished Property, then

the QI could "PARK" the title with the QI's Exchange Accommodation Titleholder (an

EAT). And later (within 180-days of the purchase) You can "buy" the title from the EAT after the Relinquished Property has been sold.

This could be a much

more expensive arrangement; because You would not only have to

Ensure Adequate

Financial Arrangements to fund the purchase by the QI's EAT before any sale proceeds are generated (You could loan it to the EAT with the Property as collateral). But also, there are

added expenses in structuring the transactions and chartering a new company to hold the title.

Often the EAT, as Owner-Landlord, "Leases" the "Parked Property" to You to possess as a Tenant

and NOT as Owner, until the Sale of the Replacement Property and Completion of the Exchange when You then take Possession as Owner.

As a first alternative to a reverse exchange You might renegotiate Your contract to buy the Replacement Property from the Seller to delay the closing until after the Relinquished Property can be sold (perhaps with a large or non-refundable deposit). Or (if feasible) you might get an "option" to buy the Property at a later date.

As another alternative to a reverse exchange Your "un-related trusted friend" could buy the Property from the Seller and contract to sell it to you after the Relinquished Property can be sold (perhaps at a premium).

An IMPROVEMENT Exchange —

Similarly, if the Taxpayer wishes to make Improvements to the Replacement Property with funds from the Exchange Account; the title to the Replacement could be "PARKED" with QI's EAT (see Reverse Exchange above) then You as Tenant might supervise the Improvements that must be completed and title transferred to You as Owner before Expiration of the 180-Day Deadline.